5 Human Behaviors Disrupting Customer Experiences & Business Models

CUSTOMER EXPERIENCESTRATEGY

There is a continuous cycle of disruptions of businesses and business models that will continue in the business world until the end of time. Our traditional ways of managing our money and doing things with our money are changing, changing fast, and changing in the long run. I have observed that there are 5 human behaviors driving customer experience requirements, forcing businesses to change or not survive. I believe they are trends because I believe what is important to us (humans), will change over time.

This article is based on the convergence of my passions: operations, technology, & human behavior/psychology, and customer experience. Human behavior is something that I have personally invested time into understanding and applied for years now.

This topic excites me as I understand that behind every piece of code, every business decision, every process design, and every customer decision are human beings. I believe human behavior & psychology is tied to leadership, motivation, company culture, understanding of process issue drivers, and most importantly as it ties to business, understanding the customer's side of this equation.

I believe there are 5 key human behavior trends that I believe are the driving force behind recent business disruptions. The companies or institutions that choose to adjust to or optimize to these 5 trends best will be best positioned, to win this zero-sum game competition. Unfortunately, this is a zero-sum game, in my opinion, there will be losers at the end of this and that loss may lead to business casualties.

Below I have listed those 5 human behaviors and tendencies, which may seem oversimplified and potentially appear cynical but it's taking the customer side down to the most simple elements and building your business model and customer experiences around them.

5 Human Behavior Trends Driving Business Disruptions

We are LAZY

We are ANTISOCIAL

We want SIMPLICITY

We want a CUSTOMIZED EXPERIENCE

We want INSTANT GRATIFICATION

We are lazy!

We do not want to drive anywhere or need to leave the comfort of our homes to accomplish things if we don’t need to. We prefer for things to be easily accessible at our fingertips with very little effort.

We are antisocial!

We prefer not to meet with people face to face if we don’t have to. We like to do it on our terms, with the people we want to. Also, if not necessary we don’t even want to talk to another person (over the phone or in person) to get what we want. If we can do or request something without needing to interact, many of us prefer that path.

We want simplicity!

We hate complexity. Long gone is the time when we are impressed by intelligent-appearing companies giving us lots of options or requiring us to think to get what we want. Anything that makes us feel remotely challenged is threatening to us and we prefer to avoid it if at all possible. I have been observing this and the concept drove me to write the book: 'Simplified Process Improvement, the art of process improvement decoded into 5 simple steps.'

We want a customized experience!

We want to feel extra special as if the experience was uniquely designed for us. This is in contrast with the desire for simplicity however, we want a customized experience but expect the companies to figure out that complexity & no need to expose us to that complexity. The key point here is, that even if it is incredibly complex to deliver a customized experience for a customer, that complexity should not be passed on to the customer.

We want instant gratification!

The more we need to wait to get what we want, the more we begin thinking about alternatives. Those alternatives include alternative solutions, alternative products, and often alternative companies. Our impatience is accelerated in this digital age. As technology improves, we simply expect everything to be faster.

We can choose to 'fight' these 5 behaviors while delivering the same 'ole and try to convince customers that they are not necessary, however, the best option is to adjust or become extinct.

I have multiple examples of the impact of these behaviors on businesses that either no longer exist or are now simply a shadow of their former selves.

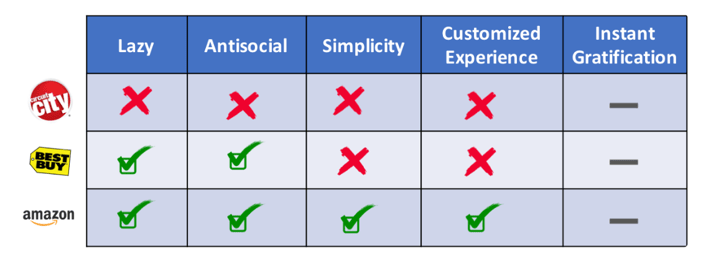

The End of Circuit City

The way I am approaching this methodology is by applying the 5 human behavioral trends and applying them to the companies or methods that did not survive or are on the way out.

Circuit City didn’t survive because it chose not to appropriately invest in e-commerce, whereas Best Buy did. Before this point, neither was really 'on the internet', but when it became imperative to do so Best Buy did. Best Buy chose to at least sell the products in their physical stores online, not a simple or idea process but at a minimum its evolution. This is the human behavior of not wanting to physically go to a store and not wanting to speak with someone to get what you want. We are now going through that transition of finding out how much longer Best Buy will survive against Amazon, which offers a simpler experience & also a more customized experience, which satisfies our need for shopping from the luxury of our homes. Even though Best Buy does offer online shopping, the web online experiences don’t even compare. The X-Factor is for the smaller audience whom if their definition of instant gratification comes from physically shopping at a store and taking it home with you that day, then Best Buy wins. Versus instant gratification coming from which the online retailer gets you your product faster online, then Amazon wins. This is the reason for the dashes in the instant gratification category because it depends on personal preferences (this may very well be what is allowing Best Buy to still be around).

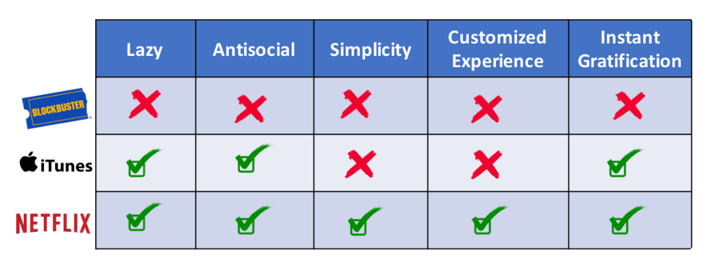

No more Blockbuster

The emergence of the phenomenon that movies could be downloaded from the convenience of your home without having to physically go to a brick-and-mortar location led to the demise of Blockbuster. iTunes and Netflix both fight in this space. Now, where I see Netflix beating out iTunes in the next wave is, in the simplicity & customer experience categories. There are a handful things that currently make iTunes not customer-focused, iTunes still requires you to buy movies individually and go through additional transactions to watch your movie. Netflix is much simpler. Netflix carries all the same benefits as iTunes, except that you can just watch what you want, when you want to stream it, and even download it at no extra purchase or extra steps (other than your monthly fee). For example, the need to make individual purchases for iTunes movies leads me to only use iTunes when there is no other option.

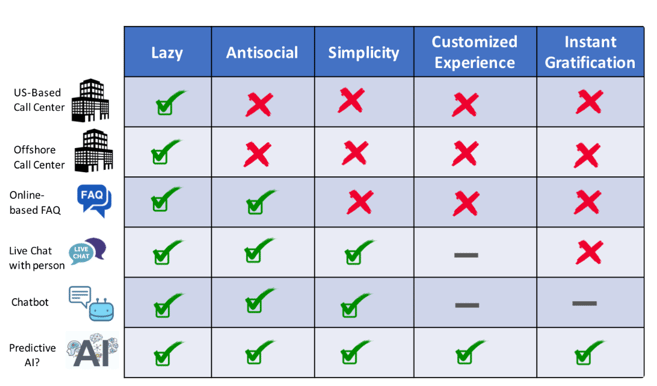

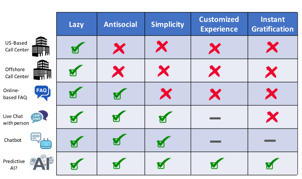

Traditional Call Centers Will Look Very Different

Call centers are not unique to any one specific type of business, they are found for most businesses that choose to provide some way for customers to communicate with the company. This space continues to evolve quickly.

Traditional call centers, which are still very much active today were originally all US-based for American companies. Then eventually to save costs, they have been sent overseas, however no improvement just a reduction in costs. Then our companies began investing heavily in their website frequently asked questions (FAQ) search functionalities so that customers can self-serve. This does help out with reducing call volumes but not a major disruptor. Then came the birth of the live chat function, the ability to chat via your computer or phone with a live person on the other end. A little simpler than searching through websites for answers as it requires less effort as you can simply just ask for what you want, but still not fully customized or instant. Next, came the emergence of the Chatbot, a similar chat functionality but instead of with a live person, with logic that mimics a person. This is similar to offshoring in that it cuts costs (of requiring a person to operate) but doesn't really improve on other elements, except maybe it is a little faster with instant responses. Though I will add that Chatbots still have limitations and 'glitches' with respect to the quality of responses I believe the next wave will come from artificial intelligence (AI). This can come in various forms and various waves, I believe eventually we will be able to predict issues before they occur and potentially address them directly before they escalate. If I were to invest in a new business model or product, it would be an AI tool that predicts customer escalations or predicts customer questions before the customers even has the need to ask them or even before the customer realizes they are going to have a question. Then combine this with programming the AI tool to solve the issue on its own too.

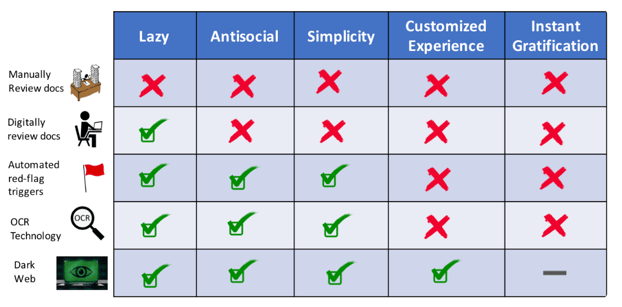

Fraud & AML will be changed forever

Fraud & anti-money laundering is an interesting angle I am taking with this. I am taking this from the internal business perspective though, where the customer is the business itself, in pursuit of improving its own experience and effectiveness.

Before, there used to be a set of 'highly-trained' detectives or fraud investigators who could smell fraud from a mile away. They would review paper documents and be able to determine based on signatures and patterns, if something smelled fishy. 🕵️♂️ Then came that same approach but instead of reviewing piles and piles of papers, trained experts would refer to scanned documents and review them in the convenience of their desktop. Then came investments in more sophisticated automated technologies of internal business systems, which simplified the process of no longer needing to scan through everything only certain things that met certain pre-defined criteria. This is a space, I worked very heavily in, with the development of detective and preventative controls in a large financial services company. Then came the resurgence of an old technology OCR (Optical Character Recognition) which is capable of determining if things are where they are supposed to be - this is good for cost savings but not much of a lift on the other elements. The latest and most recent improvement in the fraud detection space is the use of AI in the Dark Web. The Dark Web is part of the internet, which most of us do not know about or even know how to access, it is a place where cybercriminals 'hang out'. 🧟♂️ The new digital innovations are now scanning the Dark Web for fraudulent and money laundering activities before they occur. In addition, using the Dark Web to understand the patterns of emerging frauds - the fraud industry itself is a continuously evolving industry. The big improvement here, as it relates to the customization of fraud detection, it is customized to each individual client whose profiles are being scanned. This customization is important as each case is unique with potentially thousands of unique combinations, which is superior to simply having for example 10 things to check for on each document.

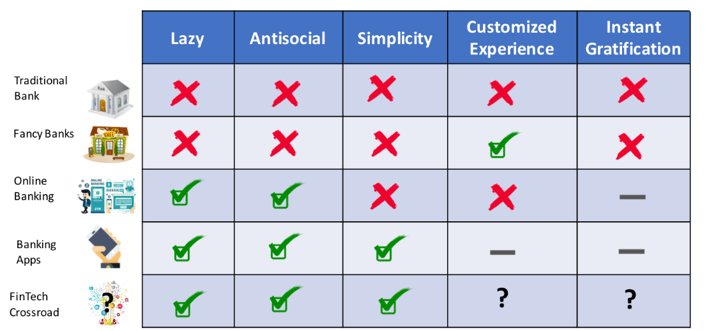

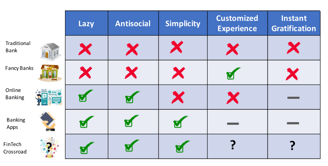

Say goodbye to brick & mortar banks

The old strategy of big banks trying to maximize their footprint by being on every corner of every street is quickly decreasing, most people no longer even visit traditional banks. The traditional brick-and-mortar bank transitioned into trying to make banks trendy & edgier by making them like coffee shops to improve the experience and offering free WiFi and coffee but still requiring us to be physically present. Then came online banking which was just attaching a website to the frontend of banks. It was a major lift but the customer experience still requires logging in and navigation to find what you want. This is similar to when taxi services simply created websites to contact & reserve the taxi but all other infrastructure was pretty much the same, which allowed Uber to swoop in and take over. Banking apps improved that logging experience and created a lift in the customized experience by letting you add your photo and then call your name out, but only partially completing the customized experience in my opinion.

This is where we are at the exciting crossroads of FinTech or TechFin.

A) Will the big banks leverage existing infrastructure but slap on a better digital customer engagement model and/or partner up with small FinTech start-ups?

B) Or will our big mega tech companies (Google, Facebook, Amazon, & Apple) utilize their existing & trusted customer-centric platforms & simply learn the ropes on the back end of the finance infrastructure?

In my opinion, the big 4 tech companies are already winning on the 5 human behavior trends and thus simply need to learn & invest in the right infrastructure to lead the TechFin charge. Especially since people’s finances are such a customer-centric experience, winning on that front gives you that edge already. Combine this with the poor reputation a lot of banks already have despite their mega efforts to appear trustworthy, their brands may already be too tarnished to survive in the long run. Again, I believe this will be a zero-sum game and a few 100-year-old banks will either not survive or end up as much smaller versions of themselves.

As a result, the financial services industry as we know it will change, where financial services professionals will have backgrounds in product management, engineering & AI instead of finance, accounting & economics. I am not rooting for one result or another, however, what I do know is that this is a part of the evolution of business. Unfortunately, I think in this race the existing big tech companies already have an unfair advantage over the big 4 banks (JP Morgan Chase, Citibank, Bank of America, & Wells).

In this situation, existing banks are trying to find ways to get more horsepower out of their gasoline-powered cars whereas the big tech companies are simply trying to figure out how to get an extension cord to connect to their electric-powered rockets. Once the rocket 🚀 is connected it is not even a fair race, again in my opinion.

These financial services innovations go so much deeper than this banking scenario, other elements I didn’t cover include big data, robo-advisers, blockchain/ cryptocurrency, learning networks, deep thinking, fuzzy logic, cloud computing, security advancements, and the API marketplace. We are almost back to the gold rush era where there is a race to be won with the landscape full of so much uncertainty yet we know change is coming at us fast.

Closing

Business is a game of survival and businesses that choose to listen to their customers, drive their business strategy around their customers, and appropriately invest to improve that customer experience deserve to survive.

These 5 human behavioral trends I have identified all lie around customer-centricity. Businesses should design their processes, hire their people, make strategic decisions, & invest in their technology around the customer experience, survival is contingent on this.

Henry Ford said it 100 years ago and it still applies today “It's not the employer who pays the wages. Employers only handle the money. It's the customer who pays the wages.”